Quick Answer: A cash-in refinance allows you to bring cash to the closing table, reducing your loan-to-value (LTV) ratio. This strategy can help you qualify for better interest rates, especially if your current LTV is high, making refinancing your Kona-Kohala Coast luxury property more accessible and cost-effective. For example, reducing your LTV from 100% to 80% on a $2 million home by bringing $400,000 to closing could unlock significant savings.

Key Takeaways: Smart Refinancing for Hawaii Luxury Homeowners

- Cash-in Refinance: Bring funds to closing to lower your LTV and secure better mortgage rates.

- LTV Impact: A lower LTV (for example, 80% or 75%) is often crucial for qualifying for competitive refinance options.

- Freddie Mac Relief Refinance: A specific program designed for homeowners with high LTVs, provided they meet strict eligibility criteria.

- Strategic Savings: Refinancing can significantly reduce monthly payments and overall loan costs on your Kona-Kohala Coast property.

- Expert Guidance: Navigating these options requires a strong understanding of luxury market nuances and lending programs.

Over nearly two decades selling luxury homes on the Kona-Kohala Coast, I’ve worked with hundreds of affluent individuals. One of the most common questions I hear is: “How can I refinance my Hawaii home if I have limited equity?”

The answer isn’t magic—it’s a system. What I call the Polimino Refinance Strategy is the result of years of testing, refinement, and proven results. Rather than simply describing the system, let me answer the three most common questions luxury homeowners ask about refinancing options. These are real questions from homeowners and the honest answers that explain exactly what we do differently.

What is a cash-in refinance, and how does it help me refinance my Mauna Kea second home?

A cash-in refinance involves bringing cash to the closing table to reduce the principal balance of your new mortgage, making the new loan smaller than the existing one. This action directly lowers your loan-to-value (LTV) ratio, which is critical for qualifying for the best refinance rates, especially for a luxury property on the Kona-Kohala Coast.

For example, if you have a $1.5 million mortgage on a $1.5 million home (100% LTV), contributing $300,000 in cash would reduce the new LTV to 80%, making you eligible for significantly more favorable loan terms. This is a core principle of the Polimino Refinance Strategy, enabling homeowners to leverage available capital for long-term financial savings.

Should I consider a cash-in refinance for my Hualalai vacation rental if interest rates are lower?

Yes. If current interest rates are significantly lower than your existing mortgage, a cash-in refinance for your Hualalai vacation rental can be a highly effective financial move. Even if property values have fluctuated, bringing cash to lower your LTV to an acceptable threshold—typically between 75% and 80%—can allow you to access more competitive interest rates.

This can translate into substantial savings on your monthly mortgage payments and over the life of the loan, improving your overall cash flow from the rental property. For example, reducing the interest rate by just 0.5% on a $2 million loan could save more than $800 per month.

What is the Freddie Mac Relief Refinance program for Hawaii homeowners, and do I qualify?

The Freddie Mac Relief Refinance – Same Servicer program offers a pathway for homeowners, including those on the Kona-Kohala Coast, to refinance even with limited or no equity. This program is designed specifically for borrowers with higher LTV ratios who want to secure a lower interest rate.

To qualify, your mortgage must be owned or guaranteed by Freddie Mac, you must be current on all payments with no missed payments in the previous 12 months, and your LTV must typically be greater than 80%. For example, if your LTV is 95%, this program may still allow you to refinance when conventional options might not.

The Bottom Line: Strategic Refinancing on the Kona-Kohala Coast

Navigating refinance options for a luxury home, particularly when equity levels fluctuate, requires a strategic approach. Whether through a cash-in refinance or a specialized program such as Freddie Mac’s relief refinance option, understanding your LTV and using capital strategically can unlock meaningful financial advantages.

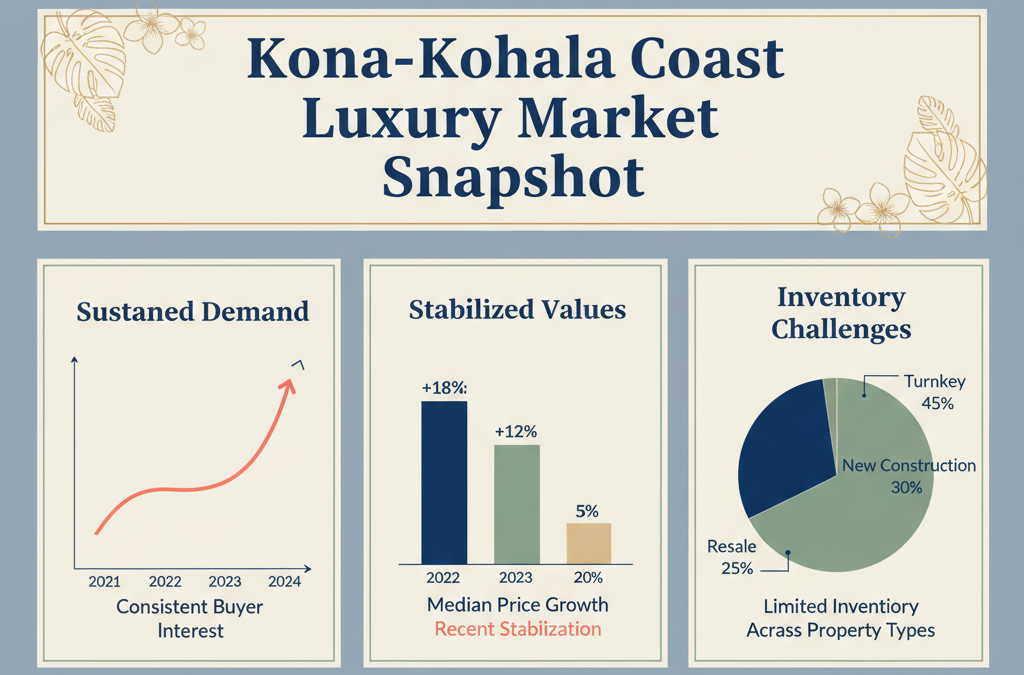

Experience in the Kona-Kohala Coast luxury market shows that proactive planning and professional guidance are critical for high-value mortgage transactions.

I would not be surprised to see more homeowners on the Kona-Kohala Coast exploring these refinancing strategies as market conditions evolve. We would be honored to be of service.

Frequently Asked Questions

Q: Who qualifies for a cash-in refinance for a Hawaii luxury home?

A: Homeowners who have available funds to reduce their loan principal and improve their LTV—typically targeting 80% or 75%—may qualify. This approach is often used by borrowers seeking lower interest rates for Kona-Kohala Coast properties.

Q: What is Loan-to-Value (LTV) and why is it important for refinancing?

A: Loan-to-value (LTV) is the ratio of the loan amount to the home’s appraised value. Lenders use this metric to evaluate risk. Lower LTV ratios, such as 80%, generally lead to better interest rates and easier approval for refinancing.

Q: Can I use funds from a 401(k) or savings account for a cash-in refinance?

A: Yes. Funds from savings accounts, retirement accounts, or other liquid assets can often be used for a cash-in refinance. However, borrowers should consult a financial advisor to understand potential tax implications.

Q: What are the risks of a cash-in refinance for my Kona-Kohala Coast property?

A: The main risk is committing a large amount of cash that could otherwise be invested elsewhere. However, securing a lower interest rate and reducing long-term loan costs may offset this concern for many homeowners.

Q: How does the NMLS protect consumers when working with a mortgage banker?

A: The Nationwide Multistate Licensing System (NMLS) regulates mortgage professionals and promotes transparency and consumer protection by requiring licensing, oversight, and accountability for mortgage lenders and brokers.